Life Insurance for Tax Free Retirement Income

Table of Contents

Leveraging Life Insurance for Tax Free Retirement.

Retirement can be a blissful phase of life, or a period filled with financial worries. It all depends on how well you prepare your financial future.

One key factor that can make a significant difference is the strategic use of life insurance.

In this article, we will explore the various ways in which life insurance can be leveraged to enhance your retirement journey. We will look into the benefits, options and considerations involved in using life insurance. So, you can achieve financial security during your golden years.

Whether you are just beginning to plan for retirement, or you are looking for new ways to maximize your tax free income, this article will provide you with valuable insights.

We will focus on :

SAVE TODAY, RETIRE YOUR WAY

Don’t Leave Your Future To Chance. Create It!

Understanding the Mechanism of Tax Free Income Generation

Retirement is a time when tax-free income can make a significant difference. Life insurance policies can be the key to unlocking that financial advantage. It not only provides a death benefit but can also serve as a valuable tool for generating retirement income.

One of the ways life insurance can contribute to tax-free retirement income is through the accrued cash value within the policy. Policyholders have the option to withdraw funds or borrow against the policy, creating a tax-free income stream. However, it’s crucial to have a thorough understanding of the policy mechanism to maximize these benefits and avoid unexpected taxes or penalties.

Think of insurance as a reliable financial ship that helps you navigate the challenges of taxes during your retirement journey.

One significant advantage of using insurance as a retirement income tool is the tax advantages it offers. The cash value inside your policy can grow tax-deferred, meaning you won’t owe taxes on any earnings as long as the funds remain within the policy.

By harnessing the potential of life insurance, you can enjoy a tax-free income stream during retirement, ensuring financial stability and peace of mind. However, it’s important to consult with professionals who can guide you through the intricacies of your policy and help you make informed decisions that align with your retirement goals.

With the right knowledge and strategy, life insurance can be your pot of gold, providing the tax advantages you need to thrive in your golden years.

Unlocking Insurance Policies for Tax-Free Retirement Income

Life insurance is not just a tool for providing financial protection to your loved ones after your passing. It can be a powerful instrument for securing your own retirement, as well.

By incorporating life insurance into your retirement planning strategy, you can create a solid foundation for a worry-free retirement.

A wide variety of insurance products can fuel your retirement income engine. Life insurance policies with cash value accumulation are an essential tool to unlock a tax-free retirement strategy. They also provide death benefits while enabling policyholders to build cash value over time, which can be accessed later in life for a regular stream of retirement income.

In your journey to generate tax-free retirement income with life insurance, it’s crucial to recognize that every insurance product carries different risks and rewards. Exploring and understanding them fully is critical to making an informed decision that aligns with your retirement goals.

Sculpting Your Retirement Income Through Tax Planning

Planning ahead for taxes can elevate your retirement from golden to platinum status.

By taking into account the potential tax implications of your retirement income strategy, you can maximize the amount of money you keep for yourself.

Utilizing insurance strategies to optimize tax-free retirement income is a wise decision. One effective approach is strategically timed withdrawals from cash-value life insurance, which can provide additional income during your retirement years. However, it's important to be mindful of the timing and sequence of these withdrawals to ensure the policy remains intact and to maximize tax efficiency.

Furthermore, safeguarding the longevity of your retirement assets is essential to ensure that you won't outlive your assets. Incorporating insurance as a key component of your plan can help minimize the tax burdens you may face by the time you retire.

By being proactive in your tax planning and leveraging insurance strategies, you can enhance the financial security and longevity of your retirement. Don't settle for a merely golden retirement when you have the opportunity to achieve platinum status by making smart decisions and optimizing your tax-free income.

Real-life Insights

Case Study and Exemplification

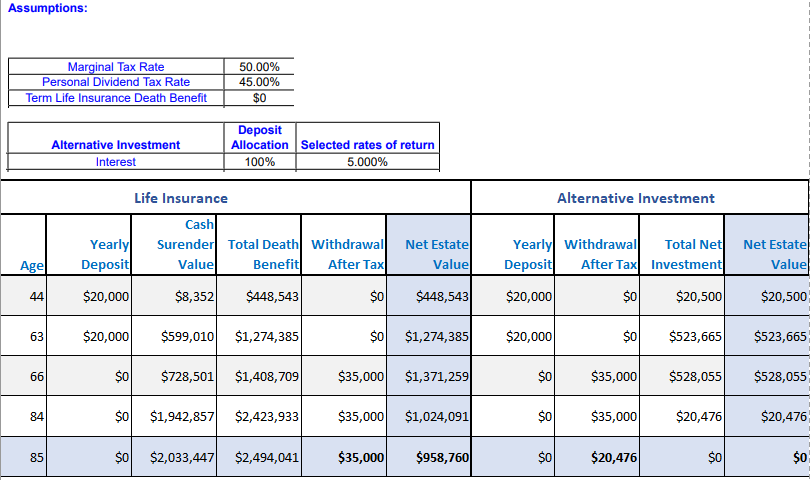

Let's examine a real-life example that demonstrates how life insurance can generate tax-free retirement income.

Meet Sandra.

Sandra is 43 years old and plans to retire at age 65.

At retirement, she wants a tax-efficient way to supplement her income with an extra $35,000 per year for 20 years while creating an estate.

She can set aside $20,000 each year for the next 20 years to accomplish her goal.

She is considering two options:

- Invest $20,000 each year for 20 years in a taxable investment and at age 65 make a withdrawal to supplement her income, or

- Transfer $20,000 each year for 20 years to a permanent life insurance policy to pay the premium and use the cash value of the policy as collateral for a bank loan.

The results

Both options are adequate to supplement Sandra’s retirement income until the age of 85.

If she opts for the first option and invests her savings in a taxable investment, she will acquire $684,476 but her heirs will not inherit anything.

Whereas, if she selects option two and uses the cash value of her permanent life insurance to supplement her retirement income, she will amass $700,000 and her heirs will receive a tax-free death benefit of $958,760.

In summary, because she saved $400,000 over 20 years ($20,000*20), both options will provide her with an annual income of $35,000 until the age of 84. However, using the Insured Retirement Program* results in a larger estate than what would be achievable with taxable investments.

*The Insured Retirement Program is a concept. It is not a product. It is based on current tax legislation which may change. This information does not constitute legal, tax, investment, or other professional advice.

Conclusion

In this case study, Sandra uses a permanent life insurance policy by leveraging its accumulated cash value as collateral for a bank loan. This strategic move provides a regular stream of tax-free income, ensuring a comfortable lifestyle during retirement and a significant death benefit for her heirs.

It shine a light on the power of life insurance as a tool for creating tax-free retirement income. And, it shows that with the right strategy and guidance, insurance can truly become a game-changer in your retirement income planning.

By exploring similar opportunities and consulting professionals, you can leverage life insurance to create a tax-efficient income stream, tailored to your unique needs.

SAVE TODAY, RETIRE YOUR WAY

Don’t Leave Your Future To Chance. Create It!

The Role of Professional Guidance in Your Insurance Strategy

As with any financial strategy, seeking professional advice is essential. Navigating the world of life insurance and retirement planning requires expertise and knowledge especially for the ever-changing tax landscape. Consulting with Financial Advisors specialized in life insurance can provide invaluable insights and help you tailor a solution that aligns with your specific needs and goals.

Another key point is that regular reviews and adjustments of your insurance strategy will be essential. Your retirement needs and the tax landscape may change over time, necessitating strategy tweaks for optimal results.

We can guide you through these complexities, ensuring that you make informed decisions and maximize the benefits of life insurance as a retirement income tool.

Conclusion

Bottom line is that life insurance can be an extraordinary tool to create a stream of tax-free retirement income. It's not just about providing a death benefit to your loved ones; it's about living benefits that can help make your retirement more financially secure. A retirement strategy that incorporates life insurance can offer an added layer of protection against the unpredictability of markets and longevity, tax efficiency, and potentially a legacy for the next generation.

Make the most out of your retirement years with a well-planned, tax-efficient strategy!

We can help you create a system that integrates life insurance into your overall retirement savings strategy. Feel free to connect with us to discuss your long-term financial plan and explore how life insurance can contribute to your retirement goals.

SAVE TODAY, RETIRE YOUR WAY

Don’t Leave Your Future To Chance. Create It!

Here are some additional resources to help you on your financial journey:

She is specialized in designing and implementing retirement strategies that prioritize your financial security. The Insured Retirement Program is just one of the strategies that she offers to help you achieve your retirement income goals. As an experienced professional, she is ready to guide you through the process, tailor a plan to your unique needs, and ensure you a comfortable retirement.

Contact her today to schedule a consultation and take the first step toward a secure and fulfilling retirement.

Disclaimer:

The Insured Retirement Program is a complex strategy, and its suitability may vary depending on individual circumstances. Consult with a qualified financial advisor for personalized advice based on your specific needs and goals.

Financiallysecure’s content is meant for general informational purposes only and should not be considered financial, tax or legal advice.