Insured Retirement Program

Table of Contents

Insured Retirement Program (IRP): Securing Your Future

Planning for retirement involves considering various strategies that can provide both insurance protection and a reliable income stream in the future.

One such strategy is the Insured Retirement Program. It is designed to meet the needs of insurance coverage and retirement income supplementation.

How does the Insured Retirement Program work?

The Insured Retirement Strategy offers a flexible and customized financial solution that can be tailored to meet your specific needs and goals. Basically, it involves complex financial considerations, and its suitability may vary depending on your specific circumstances.

Here are the steps of the Insured Retirement Strategy:

- 1. Purchase a specially designed life insurance policy:

The first step is to acquire a specially designed life insurance policy that aligns with your own needs and financial goals. This policy will serve as the foundation for the strategy.

- 2. Implement the process:

The second step is to implement the process. The IRP program is not about the product it’s about the process that uses a specially designed product. You start accumulating cash value inside your policy. The cash value accumulation is based on the extra deposits that exceed the policy’s premium up to the maximum allowable limits. By doing so, you maximize the cash value component of your policy, which grows on a tax-deferred basis.

- 3. Supplement your retirement Income:

The third step is to use the policy as collateral for a loan from a third-party lending institution. When you reach retirement age and require additional income, instead of directly withdrawing funds from the life insurance policy, you can use the policy as collateral for a loan. As with all the other loans, this loan is tax-free too. This allows you to access the funds and supplement your retirement income without triggering a taxable event.

- 4. Loan Repayment and Death Benefit:

The final step, upon your passing, the outstanding loan balance is repaid using the insurance proceeds from the policy’s death benefit. Basically, any remaining funds beyond the loan repayment amount are then distributed to your designated beneficiaries and they are not subject to taxation.

SAVE TODAY, RETIRE YOUR WAY

Don’t Leave Your Future To Chance. Create It!

Who is the Insured Retirement Program for?

It is important to recognize that an insured retirement program may not be suitable for everyone.

Generally, each Canadian’s financial situation and goals differ, making it crucial to carefully assess your unique circumstances before implementing such a strategy.

The Insured Retirement Program is ideally suited for Canadians who:

- Need Permanent Life Insurance Protection:

The program offers life insurance coverage along with the benefits of retirement income supplementation.

- Aged between 30 to 55, in a good health:

The program is most suitable for individuals in good health within the age range of 30 to 55.

- Are in a High-Marginal Tax Bracket:

Those who are in higher tax brackets can benefit from the tax advantages provided by the program.

- Desire Tax-Free Supplemental Retirement Income:

The program allows you to receive tax-free dollars to supplement your retirement income.

- Have Maximized RRSP/Pension Plan Contributions:

Individuals who have maximized their RRSP or pension plan contributions and want to explore additional retirement income options.

- Wish to Reduce Current Tax Liabilities on Investments:

By utilizing the Insured Retirement Program, you can potentially reduce the amount of tax paid on your investments.

SAVE TODAY, RETIRE YOUR WAY

Don’t Leave Your Future To Chance. Create It!

*You should consult with a knowledgeable financial advisor that can help you evaluate whether an insured retirement plan aligns with your long-term objectives. They can provide guidance on optimizing your retirement strategy so that you can make informed decisions.

Case Study: Exploring the Benefits of an IRP

To understand the benefits of the Insured Retirement Program, let’s consider an example.

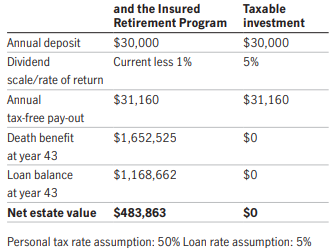

Meet John and Mary, a non-smoking couple aged 48 and 47. Currently, they require $750,000 of life insurance coverage. They plan to deposit $30,000 into the life insurance policy for the next 10 years. Looking ahead, they plan to retire in 23 years. They estimate that during retirement they might need an after-tax income of approximately $31,000 per year from non-registered sources.

THE RESULT:

With the Insured Retirement Program, they can receive tax-free loans from year 23 to year 43, amounting to $31,160 each year. These tax-free loans provide them with a powerful tool to supplement their retirement income while enjoying the flexibility to utilize the funds as they see fit.

However, they can consider an alternative investment strategy involving taxable investments instead of embracing the Insured Retirement Program.

Let’s explore the comparison:

By implementing the Insured Retirement Plan strategy, they gained several benefits:

- Steady Retirement Income:

Basically, the Life Insurance policy, when accessed in retirement, provides a reliable income stream that complemented their other retirement savings. This ensured that they could maintain their desired lifestyle without worrying about outliving their savings.

- Financial Protection:

The death benefit provided by the policy offered financial protection for their beneficiaries. In the event of their untimely passing, their loved ones would receive a lump sum payout, helping to alleviate any potential financial burdens.

- Tax Efficiency:

Moreover, by utilizing the tax advantages of the policy, they could manage their tax liabilities effectively. The tax-deferred growth of their cash value and the ability to structure withdrawals strategically allowed them to optimize their retirement income while minimizing their tax obligations.

Bottom line, the Insured Retirement Program offers them significant advantages:

- tax-free loans during their retirement years,

- a death benefit for financial protection, and

- higher net estate value.

By leveraging this program, they can secure their future and enjoy a worry-free retirement.

SAVE TODAY, RETIRE YOUR WAY

Don’t Leave Your Future To Chance. Create It!

*Please note that the figures mentioned in the case study are for illustrative purposes only. The specifics of any insured retirement program would depend on the individual’s unique circumstances, goals, and financial situation.

The Tax Implications of an Insured Retirement Program

When considering an insured retirement plan (IRP), it’s essential to understand the potential tax implications involved.

While the specific tax treatment can vary based on individual circumstances and the particular plan structure, here are some general tax considerations to keep in mind:

Contributions:

Contributions made to an insured retirement plan are typically made with after-tax dollars. Unlike other retirement vehicles like RRSPs (Registered Retirement Savings Plans) where contributions may be tax-deductible, IRP contributions do not provide immediate tax benefits.

Tax-Deferred Growth:

The cash value component of an insured retirement program grows on a tax-deferred basis. This means that you do not pay taxes on the growth as it accumulates within the policy. However, it is important to note that taxes will be due upon withdrawal or other distributions from the plan.

Tax-Free Loans:

When you retire and choose to utilize your policy as collateral for a loan, the borrowed funds obtained through the loan are typically tax-free. This provides a significant advantage, as it allows you to access additional income without incurring immediate tax liabilities.

Loan Repayment and Death Benefit:

Upon your passing, the outstanding loan balance is repaid using the insurance proceeds from the policy’s death benefit. This means that any remaining funds beyond the loan repayment amount are then distributed to your designated beneficiaries. These distributions are generally not subject to income tax, as long as they are taken as loans and not withdrawals.

Withdrawals and Taxation:

If you decide to take a withdrawal directly from the policy instead of using a loan, for instance, it is important to consider the tax implications. The portion of the withdrawal that represents the growth of the cash value is typically subject to income tax. However, the portion that represents your original after-tax contributions may be tax-free.

*Please be aware that the tax laws can change over time, and the specific tax implications of an insured retirement plan can vary depending on factors such as your province and individual circumstances.

In order to understand the specific tax implications of an insured retirement plan based on your unique circumstances it is highly recommended to consult with a financial advisor who can help you apply the IRP strategy according to the up to date tax law and regulations.

Why does the Insured Retirement Program work?

The Insured Retirement Program is a unique financial strategy that combines the benefits of life insurance protection with the opportunity to create a cash value that grows on a tax-deferred basis.

Actually, this strategy is designed to meet your current need for insurance coverage while providing you with a reliable source of income in your retirement years.

When planning for your retirement, there are many advantages to using this strategy :

Insurance Protection:

The program provides much-needed life insurance protection to ensure the financial security of your loved ones.

Tax-Deferred Growth:

By depositing excess amounts into the policy, you can create a cash value that grows tax-deferred, potentially maximizing your savings.

Loan Security:

The insurance policy acts as collateral to secure a loan from the Insurance Company, offering you financial security during retirement.

Tax-Free Borrowed Funds:

The borrowed funds are received tax-free, allowing you to supplement your retirement income without incurring additional taxes.

Loan Repayment:

At death, the insurance proceeds are used to repay the line of credit, ensuring the loan balance is settled, and any remaining amount is passed on to your beneficiaries tax free.

Conclusion

Bottom line, the Insured Retirement Strategy involves complex financial considerations, and its suitability may vary depending on individual circumstances.

Also, it offers a flexible and customized financial solution that can be tailored to meet your specific retirement income needs and goals.

To implement the Insured Retirement Program, you purchase a specifically designed life insurance policy and accumulate cash value by depositing amounts exceeding the policy charges. When you retire, the insurance policy is utilized to secure a loan, structured as a line of credit, from a financial institution. The borrowed funds are received tax-free and can be used to supplement your retirement income. At the time of your passing, the insurance proceeds repay the line of credit, ensuring financial stability for your beneficiaries.

We can help you create a system that integrates life insurance into your overall retirement savings strategy. Feel free to connect with us to discuss your long-term financial plan and explore how life insurance can contribute to your retirement goals.

Here are some additional resources to help you on your financial journey:

She is specialized in designing and implementing retirement strategies that prioritize your financial security. The Insured Retirement Program is just one of the strategies that she offers to help you achieve your retirement income goals. As an experienced professional, she is ready to guide you through the process, tailor a plan to your unique needs, and ensure you a comfortable retirement.

Contact her today to schedule a consultation and take the first step toward a secure and fulfilling retirement.

Disclaimer:

The Insured Retirement Program is a complex strategy, and its suitability may vary depending on individual circumstances. Consult with a qualified financial advisor for personalized advice based on your specific needs and goals.

Financiallysecure’s content is meant for general informational purposes only and should not be considered financial, tax or legal advice.